A cyclical consumer staples stock?

I should write about Petrobras and my huge capital gains, ride the hype to attract readers, or highlight my indecent portfolio performance over the last 15 months (thanks Petrobras and JEPQ). But when you’re aiming for the long term, you’re always interested in the next move. Yet my portfolio is light on consumer staples, for the simple reason that yields are typically low in this sector. So when a quality company shows a yield above 6% with dividend growth, I believe you have to consider it seriously—provided the long-term economic prospects are sound. Is this the case for Pernod-Ricard, the world’s number two spirits group? Or are Pernod-Ricard investors all drunk? Let’s dive in.

I/ The observation: a sharp share price decline, a corresponding yield increase

A/ All global leaders are suffering and the correction is severe

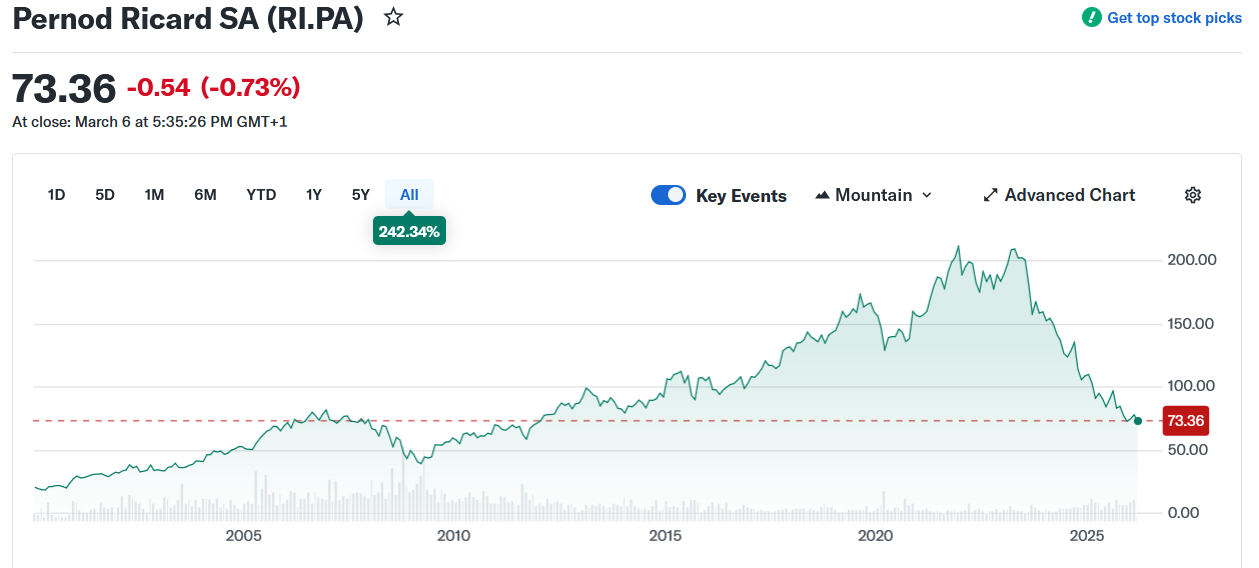

Pernod-Ricard, the French spirits giant, has experienced significant share price weakness. The chart below leaves no room for ambiguity: the current price is roughly where it stood in 2012. The decline has been pronounced, accelerating further following the publication of first-half results in February 2026. The most frequently cited explanations point to difficulties in the Chinese and American markets. But this is a global player, and a global analysis is required.

Source: Yahoo Finance

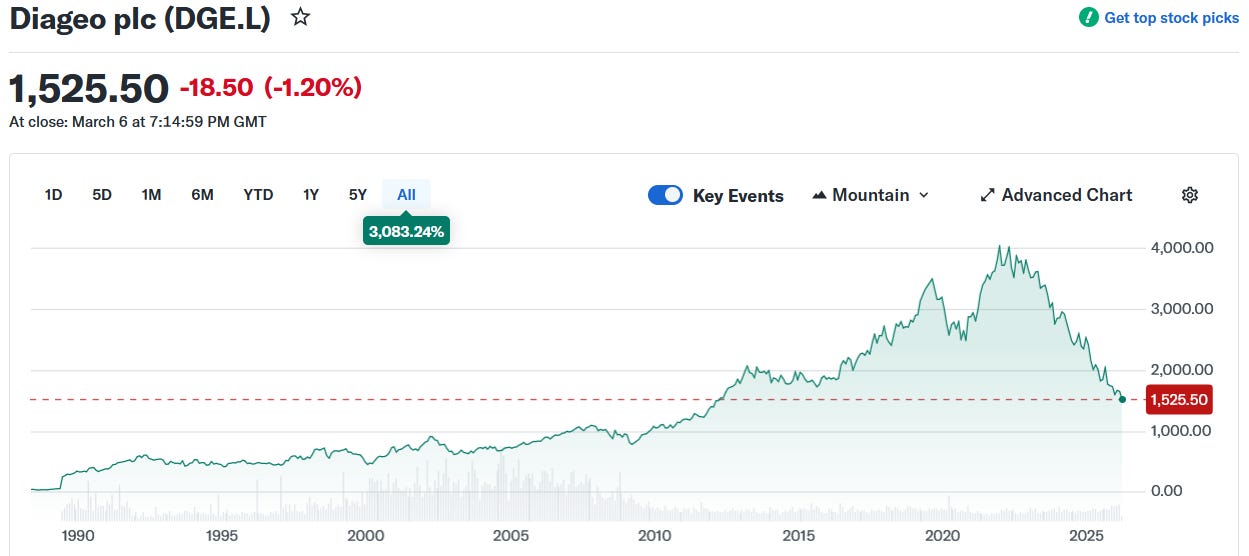

The world’s number one, Diageo, is also suffering, and its chart tells a similar story. This suggests a market-wide issue: investors believe these companies are under pressure and that short-term prospects, at least, remain weak.

Source: Yahoo Finance

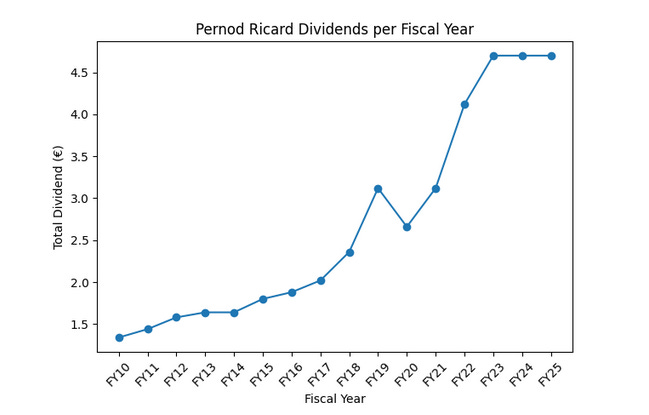

Examining the dividend history reveals that while Pernod-Ricard is not a dividend aristocrat—having reduced its payout in certain years—it is clearly a dividend grower.

Dividend growth has been less explosive for Diageo. But stepping back, the total return picture is what matters most.

B/ A mediocre total return over the last 15 years

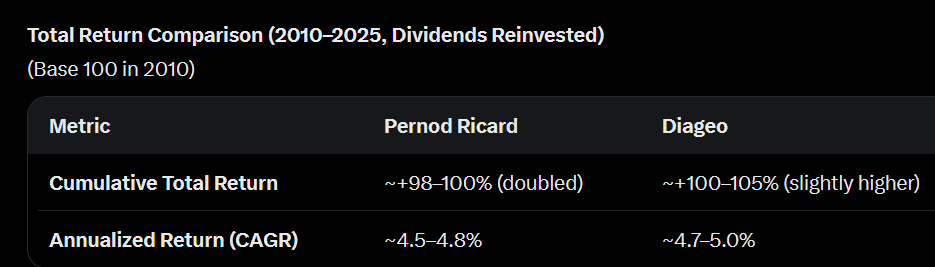

From 2010 to 2025, the total return of Pernod Ricard and Diageo was remarkably similar. Both companies delivered roughly double the initial investment when dividends are reinvested, corresponding to an annualised return of around 4.5–5%. While Pernod Ricard experienced stronger dividend growth over the period, Diageo benefited from a more stable share price trajectory. As a result, the overall performance converged despite different return drivers. In total return terms, neither company clearly outperformed the other over the 2010–2025 period. This historical record is hardly reassuring.

II/ The sector’s great hangover

A/ Cyclical difficulties

The major distillers are nursing a brutal, multi-year hangover. For Diageo, Pernod Ricard, and Rémy Cointreau—empires built on Scotch, Cognac, American whiskey, and other aged brown and white spirits—the post-pandemic party ended abruptly, leaving massive oversupply and shattered growth assumptions.

What went wrong. After explosive demand during lockdowns and the 2021–2022 recovery (driven by at-home premium drinking), volumes crashed. Distributors and retailers, who over-ordered amid the boom, are now aggressively destocking. The sector faces a historic glut: the five largest listed producers (Diageo, Pernod Ricard, Campari, Brown-Forman, and Rémy Cointreau) hold roughly $22 billion in unsold aged inventory—the highest level in over a decade. This has forced production pauses (e.g., Jim Beam halting output for all of 2026), price concessions, and repeated profit warnings. Diageo now guides full-year fiscal 2026 organic net sales down 2–3% (with operating profit flat to low-single-digit growth). Pernod Ricard reported H1 fiscal 2026 organic sales down 5.9% (to €5.253 billion), with the Americas down 12% (US down 15%) and China down 28%. Following these results, the stock fell more than 30% as investors recalibrated expectations for a longer, more uncertain recovery.

Cyclical pressures: the immediate storm. The current downturn is, in part, a classic inventory correction amplified by macroeconomic headwinds. The destocking cycle—distributors working through the mountains of cases they ordered during the demand surge—has created a self-reinforcing slump in orders. Compounding this, persistent inflation and elevated interest rates have squeezed discretionary spending across Western markets. Consumers are trading down from premium tiers or moderating consumption entirely. In the United States, soft sentiment and high borrowing costs have curbed the premiumisation trade that fuelled years of growth; tequila brands like Don Julio have been notably hit. In China, the picture is bleaker still: economic uncertainty, weakened consumer confidence, and government austerity measures limiting high-end gifting and on-trade consumption have crushed demand. Trade barriers—notably the 34.9% anti-dumping tariffs on EU Cognac—have exacerbated the collapse, with Cognac and baijiu segments suffering double-digit drops.

B/ Structural headwinds: the long fade

Beneath the cyclical turmoil lies a more fundamental realignment of alcohol consumption. The old growth engines are sputtering not just from temporary weakness, but from lasting shifts in behaviour. Mature markets (North America and Western Europe) are approaching saturation; the decades-long premiumisation trend (trading up to higher-priced spirits) has slowed and, in some segments, reversed. More ominously for the industry, younger cohorts are turning away from alcohol altogether. The rise of “sober-curious” culture, heightened health awareness among Gen Z and Millennials, and the proliferation of sophisticated low- and no-alcohol alternatives (alongside RTDs and craft beer) are steadily eroding traditional spirits volumes. These are not cyclical quirks that will vanish with the next economic upturn; they represent a durable shift in consumer preferences that the industry must navigate for decades to come.

The long view. From 2010 to end-2025, the spirits sector delivered only modest total returns. This lagged far behind the S&P 500’s ~13–14% annualised return over comparable periods. The reasons are threefold. First, valuation compression: multiples expanded sharply during the 2010s growth phase and the post-COVID premiumisation hype, then contracted violently (share prices have fallen more than 40% from their 2021–2022 peaks). Second, market saturation in mature regions, with growth increasingly reliant on emerging markets that have since faltered—China most conspicuously. Third, persistent volatility: strong dividend growth cushioned returns, but price performance suffered from repeated demand busts and inventory cycles.

The iconic brands endure. Balance sheets remain relatively solid, despite elevated leverage from carrying excess aged stock. Diversification into non-alcoholic innovation and RTDs offers some upside. Yet the old narrative of relentless ascent has given way to a more sober reality: a prolonged grind with cyclical recovery potential, but lasting structural headwinds from the slow, quiet withdrawal of a generation from alcohol.

III/ So can we bet on a sector rebound by investing in Pernod-Ricard?

A/ Pernod-Ricard is a cyclical global player; it fits a global income portfolio

1/ A global brand portfolio

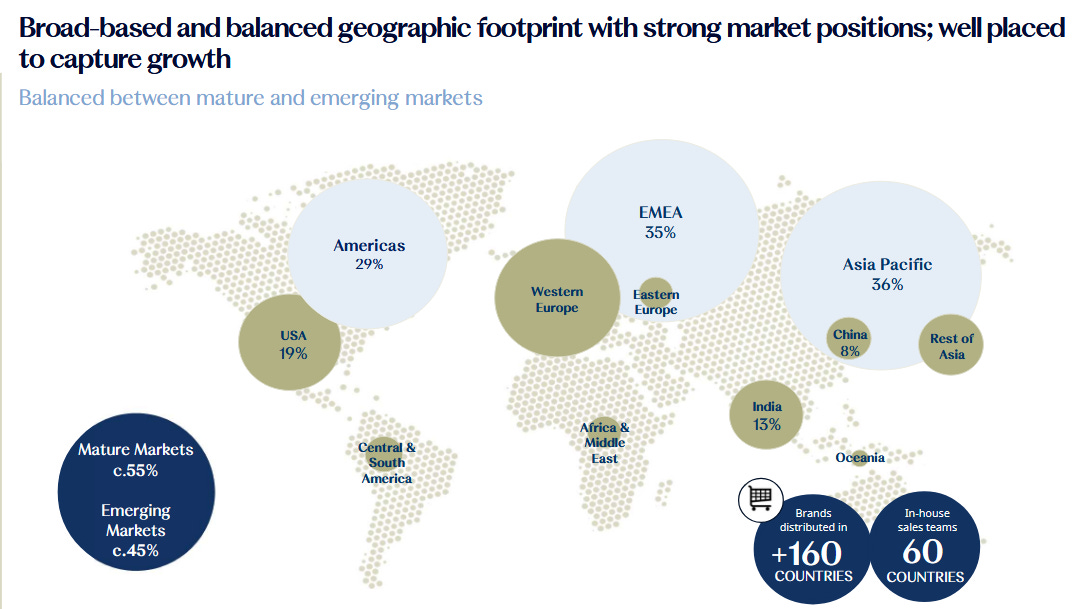

Pernod-Ricard sells everywhere in the world, and its global footprint, in the simplest terms, is divided into three roughly equal regions: the Americas, EMEA, and Asia. Within each region, there are mature—even saturated—markets alongside others still growing.

Source: Pernod Ricard H1 FY26 Financial Communication

Growth is located almost exclusively in emerging markets. (Notably, the Nordics and Japan still offer growing markets.).

Source: Pernod Ricard H1 FY26 Financial Communication

The portfolio of global brands is impressive. At this stage, I see a global business established everywhere with world-class brands. When the cyclical problems abate, I believe this company is positioned to benefit.

Source: Pernod Ricard H1 FY26 Financial Communication

2/ Global problems

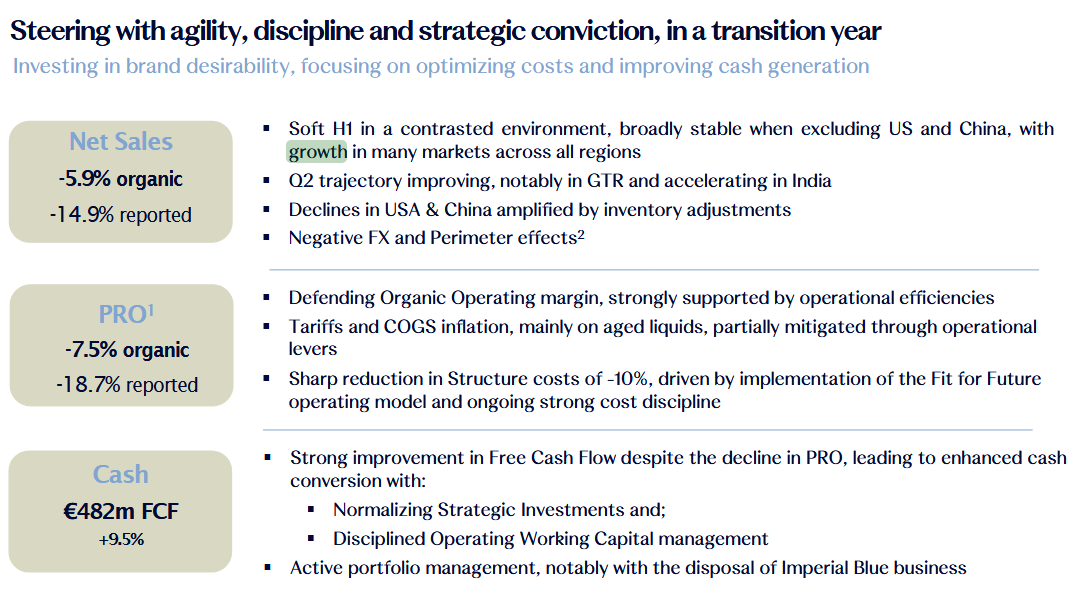

In the first half of fiscal 2026, Pernod Ricard faced a challenging transition year shaped by two distinct sets of headwinds. First, a sharply unfavourable foreign exchange environment significantly weighed on reported results, with adverse currency movements—primarily the depreciation of the US dollar, Indian rupee, and Turkish lira against the euro—combined with perimeter effects from strategic disposals such as Imperial Blue, widening the reported net sales decline to -14.9% (versus -5.9% organic). Second, the group encountered a pronounced cyclical slowdown in global demand, concentrated in its two largest markets: the United States, where organic sales fell -15% amid persistent softness in the spirits sector, weak consumer sentiment, and amplified distributor inventory destocking; and China, down -28% due to macroeconomic weakness, depressed consumer confidence, tighter regulations on premium on-trade channels, and inventory corrections. Excluding these two markets, performance remained broadly stable, with notable growth in high-potential regions such as India and accelerating momentum in global travel retail during the second quarter.

Source: Pernod Ricard H1 FY26 Financial Communication

B/ Global perspectives are not so negative

1/ Markets may rebound

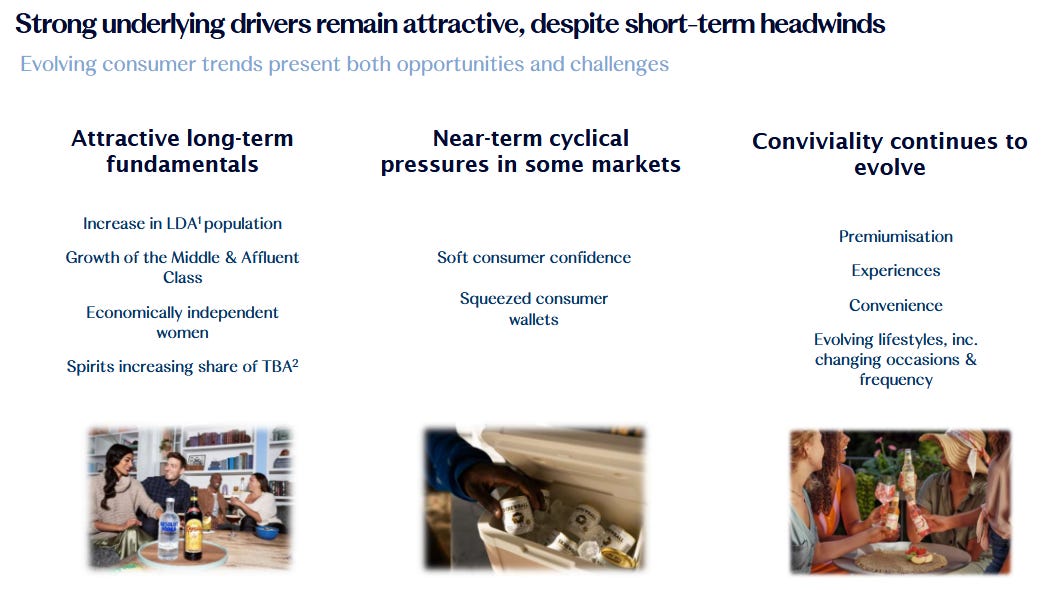

Long-term fundamentals remain attractive despite short-term cyclical headwinds in certain markets. On the positive side, key structural drivers include a growing Legal Drinking Age (LDA) population, the expansion of the middle and affluent classes, rising economic independence among women, and spirits steadily gaining share in total beverage alcohol (TBA) consumption. In the near term, however, challenges persist from soft consumer confidence and squeezed wallets amid economic pressures. Meanwhile, conviviality is evolving with consumer trends shifting toward premiumisation, a focus on meaningful experiences, greater convenience, and changing lifestyles that alter drinking occasions and frequency—trends that present both opportunities and adaptation challenges for the group. Accompanying images illustrate social gatherings with Pernod Ricard brands, reinforcing the enduring appeal of shared moments while navigating these contrasts. Overall, this underscores the company’s confidence in resilient underlying growth drivers to support recovery beyond the current transition phase. The consumer is evolving.

Source: Pernod Ricard H1 FY26 Financial Communication

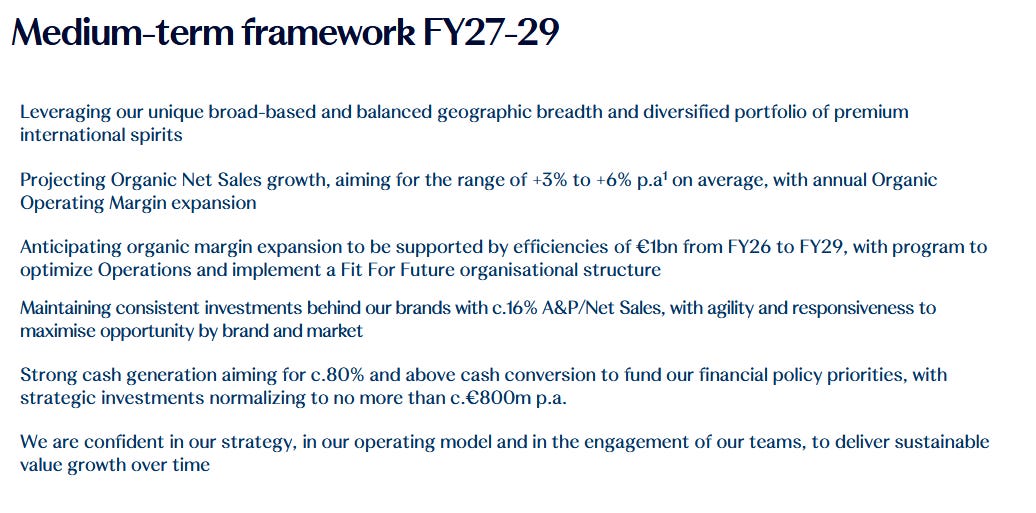

Management remains reasonably optimistic and anticipates moderate revenue increases in the medium term. For my part, I’m betting on the long term and believe the market will grow in an ageing world, with demographics remaining the central question—a subject on which nobody truly understands anything today, I fear. Older people drinking quality products? I believe in it somewhat, and that bodes well for Pernod-Ricard.

Source: Pernod Ricard H1 FY26 Financial Communication

2/ Long-term financial fundamentals are sound

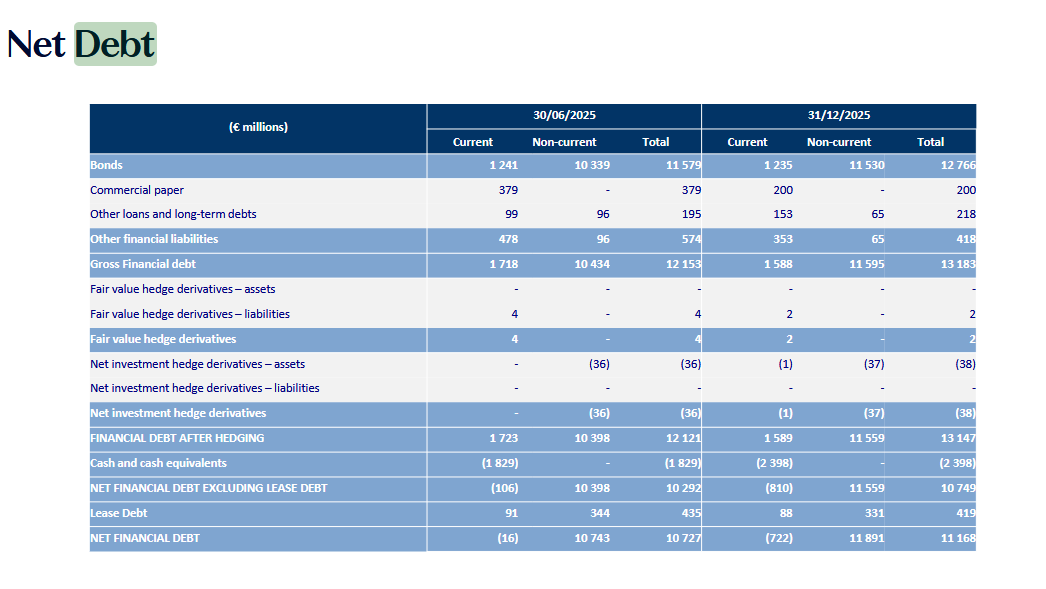

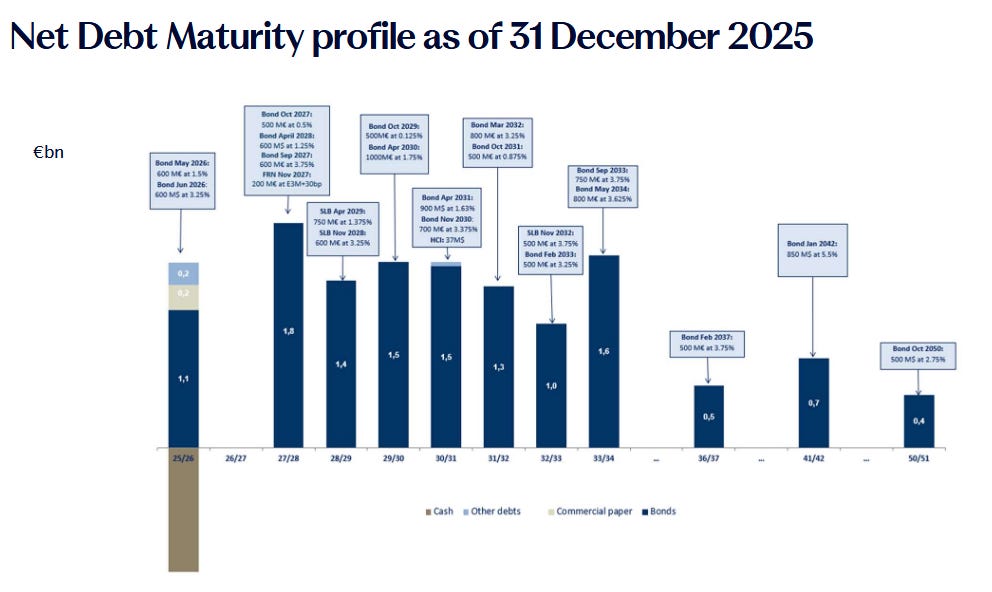

Pernod Ricard maintains a solid long-term financial position, characterised by a strong balance sheet, disciplined capital allocation, and a clear deleveraging trajectory. As of December 31, 2025 (end of H1 FY26), net debt stood at €11.168 billion, reflecting a substantial €900 million reduction over the prior 12 months—driven by improved free cash flow generation, proceeds from margin-accretive disposals like Imperial Blue, and ongoing efficiency measures—while the net debt to EBITDA ratio was 3.8x (at average rates), a modest increase due to softer EBITDA from FX and cyclical pressures but still manageable within the group’s historical norms and far below peak levels seen in prior cycles. The H1 FY26 results further confirm this resilience, with free cash flow rising 9.5% to €482 million despite a decline in profit from recurring operations, thanks to normalised strategic investments, disciplined operating working capital management (boosting cash conversion to 61%, up 11 points), and proactive portfolio optimisation. Looking ahead, the company targets bringing leverage below 3x by FY2029 through continued cash focus and expected profit recovery, underscoring a robust foundation for sustained shareholder value in the medium to long term.

Source: Pernod Ricard H1 FY26 Financial Communication

Source: Pernod Ricard H1 FY26 Financial Communication

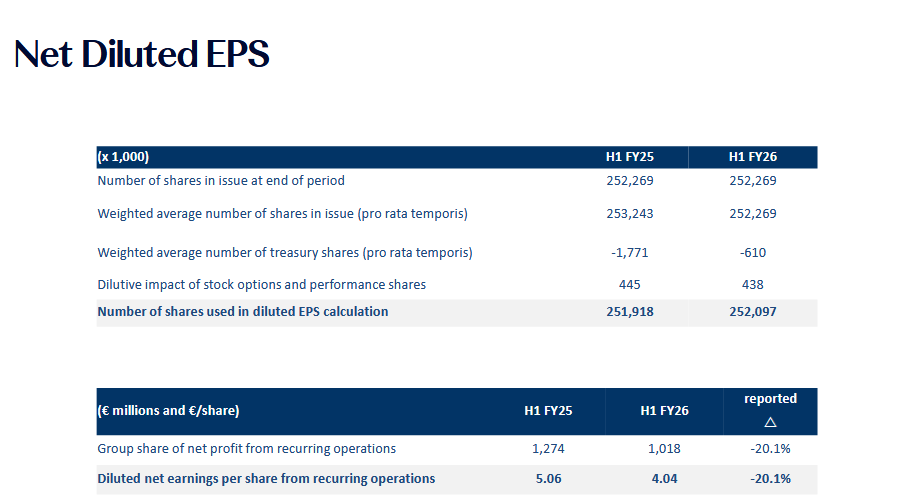

Pernod Ricard currently trades at an attractive valuation, with shares around €73 as of early March 2026, reflecting a trailing twelve-month P/E ratio of approximately 13x—significantly below its 10-year historical median of around 24-25x and well discounted compared to European consumer staples peers often trading at 17-20x. This low multiple stems from near-term cyclical pressures on earnings, with EPS impacted by the transitional year, yet the group delivered resilient free cash flow of €482 million in H1 FY26 (+9.5% YoY) despite softer profit, achieving strong cash conversion of 61% (+11 points) through disciplined working capital and normalised investments. Analysts’ consensus points to an average price target of around €94-96 (with highs up to €120-128), implying substantial upside potential of 25-30% or more, supported by expectations of profit recovery, ongoing deleveraging (target below 3x net debt/EBITDA by FY29), and structural drivers like premiumisation. Overall, these metrics suggest the stock appears undervalued at current levels, offering a potentially attractive entry point for a long-term investor betting on the group’s medium-term rebound.

Source: Pernod Ricard H1 FY26 Financial Communication

Investment takeaway

Pernod-Ricard investors are not drunk… but they have taken a serious hit. The February 2026 selloff, following weaker-than-expected first-half results, pushed the stock to levels not seen in over a decade. In my opinion, this represents a good—though still risky—entry point for my portfolio. I plan to purchase shares as soon as I have fresh cash available, likely in April.

What is my thesis? I can invest in the consumer staples sector, in a global company, with a 6%+ yield. And as a bonus, prospects for dividend growth. On the other hand, I do not believe for a second in explosive growth potential. This is a solid core holding—somewhat cyclical, and one that will need to regain its financial health.

I believe Pernod-Ricard is a suitable investment vehicle for my Pipart global income secondary portfolio. Long term—because that is my only perspective—I am counting on the dividend rising slightly, above inflation, and on a valuation returning towards historical standards, which will provide a capital cushion. Almost high yield, almost high risk, but nothing explosive. In short, an investment for the lower end of the spectrum in my global income portfolio—reserved for my secondary “lower income” portfolio (though 5% minimum all the same).

Liked this Deep-Dive? Buy Me a Coffee!

Your support keeps this newsletter independent and research-driven. If this analysis saved you time or gave you a new investment idea, consider making a one-time donation. Every contribution helps me maintain part of the research free and accessible to everyone.