What The m-REITs are made of

Oct 21, 2025

Mortgage REITs look like yield machines — but under the hood, they’re leveraged bond funds walking a tightrope. Yet, tens of billions are invested in them, even as everyone knows that their Net Asset Values (NAV) are in a structural decline and their dividends are shrinking. Are these investors completely insane? Or are they aiming for a positive total return over the long term, despite the interest rate cycles? The problem is that few truly understand their business model, yet everyone has an opinion on these rather unique investment vehicles. Let’s see what we can learn by examining the results of one of the largest players: AGNC (American Capital Agency).

I/ A tightrope walker business model

A/ Mortgage REITs for Dummies: How They Work

If you want to understand the business, here’s a breakdown of the key chronological steps.

Step 1: Raising Capital (the Beginning). It all begins with shareholders. AGNC raises funds by issuing shares, for example through a public offering. This money constitutes its share capital, or “equity.” This is the company’s own financial base, its initial fund.

Step 2: Massive Borrowing (The Leverage). AGNC does not rely solely on its own capital. To amplify its investment capacity, the company engages in massive borrowing, primarily through the repurchase agreement (”repo”) market. In practice, AGNC takes a portion of its capital to a bank and borrows a multiple of that amount—for example, eight times the initial sum. In return, it must provide assets as collateral, typically the MBS it acquires. These loans are very short-term (often overnight or a few days) and carry a variable interest rate, directly linked to benchmark rates. The result is significant leverage: the starting capital is multiplied, allowing AGNC to operate with a much larger financial pool.

Step 3: The Investment (The Asset). Backed by the raised capital and debt, AGNC acquires its primary asset: agency Mortgage-Backed Securities (MBS). These are bonds backed by thousands of US residential mortgages, guaranteed by agencies like Fannie Mae or Freddie Mac. These assets have three key characteristics: they are long-term (typically 30 years), exempt from credit risk thanks to the agency guarantee, and income-generating, as they pay a fixed interest, known as a coupon.

Step 4: Generating Income (The “Spread”). The core of AGNC’s business model lies in generating net interest income, or the “spread.” Two financial flows are at play: on one side, the cash inflows from the coupons received on the MBS portfolio; on the other, the cash outflows corresponding to the interest paid on the debt incurred. The difference between these two flows constitutes the net spread. Even if this spread is relatively small as a percentage, the leverage effect allows it to be applied to a substantial asset base, thus generating an attractive return on the initial equity.

Step 5: Risk Management (The “Hedge”). The “borrow short to invest long” model is inherently risky, particularly in the face of interest rate fluctuations. To protect against this risk, AGNC actively uses derivative instruments, such as interest rate swaps. Schematically, these tools allow it to convert a portion of its variable-rate debt into a fixed financial expense. This hedging strategy aims to stabilize borrowing costs and protect the profitability of the spread, although it does not completely eliminate risk.

Step 6: Distribution (The Dividend). As a Real Estate Investment Trust (REIT), AGNC is legally required to distribute at least 90% of its taxable income to its shareholders. The dividends—often paid monthly and characterized by a high yield—are primarily funded by the net interest spread, after deducting hedging costs and operational expenses. This is the mechanism that attracts investors seeking regular income.

B/ When Interest Rates Move: The Double-Edged Sword for m-REITs

Interest rates are the dominant force in an m-REIT’s universe. Here’s what happens when that environment shifts.

Scenario 1: Rising Rates — The Direct Threat

- Funding Costs Spike: m-REITs like AGNC rely on short-term borrowing. When rates rise, their cost of funding increases immediately, compressing the net interest spread, the core of their earnings. This directly pressures their ability to sustain dividends.

- Asset Values Fall: As new bonds offer higher yields, the market value of existing fixed-rate MBS falls. This erodes the Net Asset Value (NAV) per share.

- Leverage Amplifies the Pain: With high leverage (7-9x equity), a small decline in the total asset value translates into a magnified loss for shareholders. The very tool that boosts returns in calm markets exacerbates losses in turbulent ones.

Scenario 2: Falling Rates — The “Friendly” Trap

- A Temporary Boost: Cheaper borrowing costs widen the interest spread, boosting near-term earnings. Simultaneously, the value of existing MBS rises, increasing NAV—a positive for the balance sheet.

- The Prepayment Problem: This is the catch. As mortgage rates fall, homeowners refinance or move, triggering early repayments. AGNC is then forced to return this capital and reinvest it into new MBS that now offer lower yields. This slowly but surely erodes the portfolio’s future income potential.

The Bottom Line

An m-REIT like AGNC is a high-yield income machine balanced on a knife’s edge.

- Rising rates hurt its margins and book value.

- Falling rates create a slow-burn reinvestment risk that undermines future dividends.

In a perfect world of stable rates, it thrives. But in the real world of constant change, the generous dividend that attracts investors is also the most vulnerable component of the total return.

II/ AGNC: not totally an income investment

A/ The AGNC Paradox: Lower and Lower NAV and Dividends, Positive Total Return

At first glance, AGNC Investment Corp.’s performance seems like a textbook yield trap. Since its IPO in May 2008, the company’s tangible net book value per common share (a proxy for NAV, adjusted for preferred stock and other intangibles) has trended downward structurally—reflecting the erosive impact of interest-rate volatility, prepayment risks, and leverage amplification during adverse cycles. For instance, According to AGNC Investment Corp.’s Form 10-Q for Q3 2025, the tangible net book value per common share declined from approximately $17.59 at year-end 2020 to $8.41 as of December 31, 2024, and further to $8.28 as of September 30, 2025. This represents a structural decline of over 50% since 2020, underscoring the “knife’s edge” balance described in the theory section—rising rates hammer asset values, while falling rates trigger reinvestment at lower yields. See the share price since inception below:

Source: Yahoo Finance

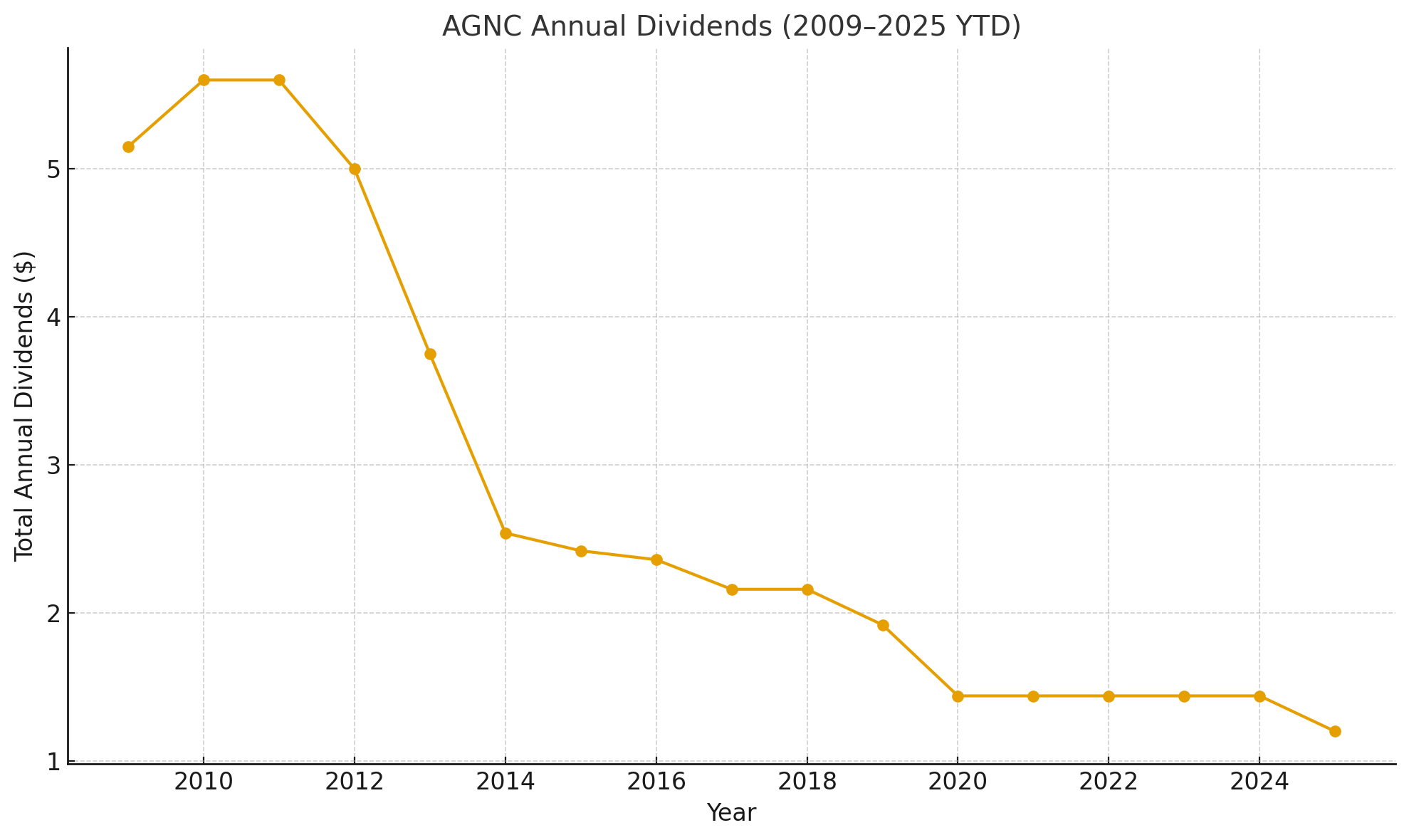

Dividends tell a similar story of contraction. AGNC’s payouts, once robust quarterly declarations exceeding $1.25 per share in 2012 (annualizing to over $5), shifted to monthly distributions but steadily shrank amid margin compression. By 2015-2016, monthly dividends hovered at $0.20 (annual $2.40), dropping to $0.16 by late 2019 ($1.92 annual), and stabilizing at the current $0.12 monthly rate ($1.44 annual) since April 2020—a reduction of more than 70% from peaks. This holds steady into late 2025, with the next ex-dividend date on October 31 for the November payment.

This trajectory aligns with broader m-REIT challenges: as spreads narrow and hedging/funding costs rise, the 90% distribution mandate forces reliance on ever-thinner net interest income, leading to repeated trims that erode the headline yield’s allure over time. Yet here’s the paradox that keeps tens of billions flowing into AGNC and its peers: total shareholder returns—with dividends reinvested—have remained positive and often resilient across cycles.

The total return tells a different story. Based on publicly-available data to mid-October 2025, $10,000 invested at IPO (May 2008) would have grown to approximately $61,000-$62,000 under dividend reinvestment — corresponding to an annualized return ~11%.

Over the past decade, annualized returns stand at approximately 6.63%, while the 5-year cumulative total return is 36.76% (about 6.4% annualized); year-to-date through October 2025, it’s a strong +22.79%. The year-by-year volatility is significant (+23.73% in 2017, +18.23% in 2016, +13.31% in 2019), yet even with the share price closing at $10.04 on October 21, 2025—well below its 2013 peak of over $20—the high dividend yield (currently 14.41%) has powered meaningful total return.

B/ What Can We Do with m-REITs in a Global Income Portfolio?

The theory and the AGNC paradox show that m-REITs are fundamentally different from traditional income investments. To use them effectively, one must consider two specific market dynamics: premium/discount to NAV and the impact of share issuance.

1. The Premium/Discount Trap and Share Dilution

The stock price of an m-REIT rarely matches its Net Asset Value (NAV), which is the underlying market value of its assets minus its liabilities.

- Buying at a Discount: The ideal time to buy is when the stock trades at a significant discount to its NAV. This means you are essentially acquiring the company’s bond portfolio for less than its liquidation value. This provides a margin of safety and the potential for capital appreciation if the stock price reverts to NAV.

- The Share Issuance Risk: When an m-REIT trades at a premium (above its NAV), the company often takes the opportunity to raise capital by issuing new shares. While this brings in funds, it is highly dilutive to existing shareholders. Issuing shares at a premium above NAV is profitable for the company, but if the premium is small, or if shares are issued when the stock is near or below NAV, the operation effectively destroys shareholder value and accelerates the structural decline of the NAV per share. This action is the main enemy of long-term investors.

2. Tactical Use: Betting on Rate Cycles

Given their sensitivity, m-REITs are not peaceful buy-and-hold investments but rather tactical plays on Federal Reserve policy.

- Best Tactical Position: m-REITs can be a compelling short-term position (1-2 years) when there is a strong expectation of a rate-cutting cycle. Declining short-term rates immediately reduce funding costs, which widens the net interest spread and boosts near-term earnings and dividend sustainability. This is a crucial window for high total returns (capital appreciation + high yield).For example, Annaly’s price surges have consistently coincided with the early to mid-phases of Fed easing cycles, when funding costs drop faster than MBS yields. Conversely, every tightening cycle (2004–06, 2013, 2022–23) has crushed spreads and valuations — proving that mREITs thrive on rate cuts, not rate hikes.

Source: Yahoo Finance

- Worst Tactical Position: Conversely, they are highly vulnerable during periods of rising rates or high volatility, as seen in the structural NAV decline.

AGNC’s price rallies have always coincided with early easing cycles (2009–2012, 2020) — when falling short-term rates and rising MBS valuations align. Its steepest drawdowns occurred in tightening phases (2013, 2022–23), when funding costs jumped faster than asset yields. mREIT income investing, therefore, is a game of timing the Fed — not time in the market.

Investment takeaway

m-Reits are not built for our philosophy of global income: you have to reinvest a large portion of your dividends, it is destroying NAV and the dividend is structurally getting down. So it is not made for me in a long term perspective.

BUT I have to admit that I love big and monthly dividends like AGNC’s ones, and that I have earned good money some years ago in markets with lowering rates. So that’s the question: will I invest some bucks in AGNC for one year or two, hoping to accumulate capital gains and fat dividends? But if I do that, will I wait for discount to NAV? I like these companies, but they are not fit for my long term portfolio. I don’t like structurally decaying NAV.

In short, too many issues and questions for a global income portfolio. But a reasonable investment for those who look for total return and DRIP each month.

Liked this Deep-Dive? Buy Me a Coffee!

Your support keeps this newsletter independent and research-driven. If this analysis saved you time or gave you a new investment idea, consider making a one-time donation. Every contribution helps me maintain part of the research free and accessible to everyone. Miracle of m-Reits

Disclaimer: This article is for informational and educational purposes only and should not be considered financial or investment advice. The views expressed are solely those of the author and do not constitute a recommendation to buy, sell, or hold any security. Always conduct your own research and consult with a professional before making any investment decisions.