Part 1 – Macro strengths

Jul 01, 2025

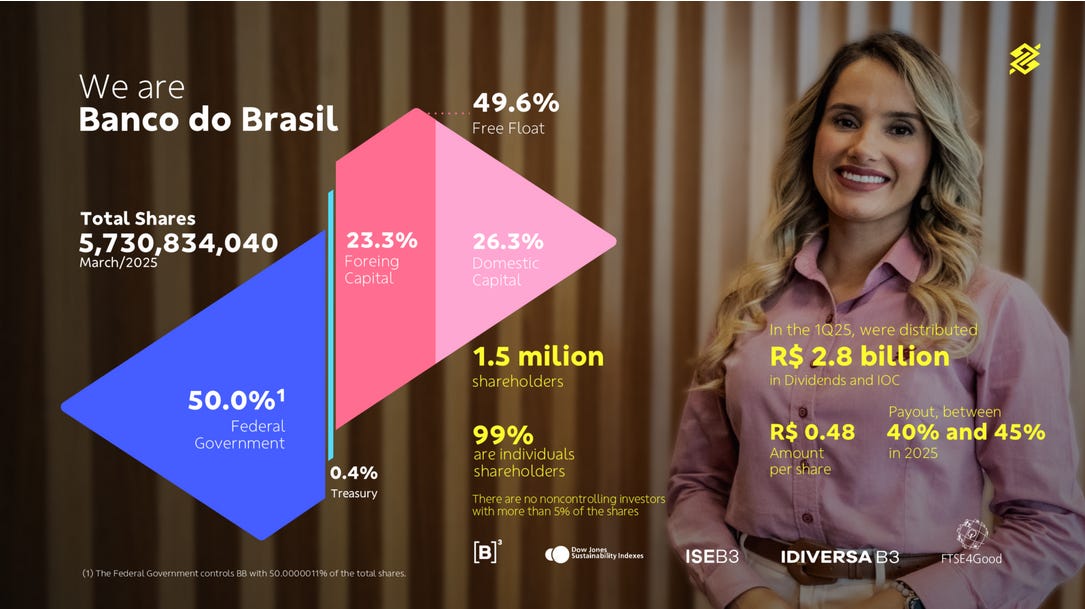

Banco do Brasil (BBAS3, BDORY as an ADR), established in 1808, stands as a major financial institution in Brazil, with 50% state ownership. Boasting a market capitalization of approximately 40 billion USD and a network of over 4,700 branches, this public bank holds a pivotal role in the Brazilian economy, serving as a key barometer of national health and commodity trends, particularly through its deep ties to the agricultural sector and export markets. Why consider a long-term investment in this entity? Let’s explore its strengths and the macro factors that might appeal to patient investors, with a special focus on its dividend potential as a cornerstone of long-term value. We’ll discuss specific risks in Part 2 next week.

I/ Banco do Brasil: A Proxy for Brazil’s Economic Health Since 1808

A/ Two Centuries of Resilience

When King John VI fled Napoleon’s invasion in 1808 and set sail for Rio de Janeiro, he didn’t just save his crown—he founded Banco do Brasil, Brazil’s oldest financial institution and one of the world’s longest-operating banks. Established to stabilize the exiled Portuguese crown’s finances and issue currency, Banco do Brasil quickly became the backbone of Brazil’s economy. From financing the nation’s first coffee exports to supporting modern agribusiness, its 217-year history reflects Brazil’s growth and resilience, making it a unique proxy for the country’s economic journey and a cornerstone for investors seeking exposure to this dynamic market.

Source: Banco do Brasil

After being liquidated in 1829, the bank was reborn in 1851 as a private entity before once again becoming a pillar of the national economy—particularly by financing agriculture, European immigration, and public finances at the dawn of the Republic. Today, Banco do Brasil remains a major force in Brazil’s economic and social development, with a strong presence in household and business lending, as well as strategic sectors, while also engaging in sustainable development and social inclusion initiatives through its foundation, established in 1985. Banco do Brasil’s history since its founding in 1808 is deeply intertwined with the economic and social development of Brazil.

B/ For the Next Decades, Banco do Brasil Is a Bet on One of the Safest Members of the BRICS

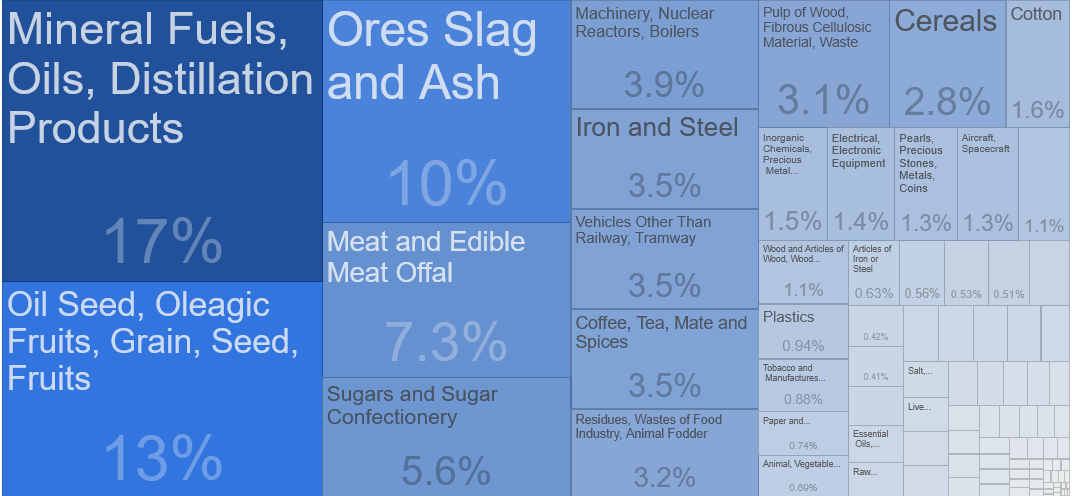

Brazil boasts powerful assets for its long-term economic future. It possesses vast natural resources, both agricultural and mineral, making it one of the world’s leading exporters of food products and strategic minerals.

Source: https://maps-brazil.com/brazil-natural-resources-map

Its young and growing population, along with a dynamic middle class, supports domestic demand and growth potential, as reflected in GDP growth of 3.4% in 2024 and projected convergence to 2.2%–2.5% in the coming years according to the World Bank and the IMF. The country is also investing in the energy transition, with major opportunities in renewables such as bioenergy and wind power. Finally, new trade agreements, such as the one with the European Union, open up export prospects and sectoral diversification. These factors provide Brazil with solid foundations to strengthen its position on the global economic stage. To conclude, Banco do Brasil is not just a proxy for Brazil’s economic future — it is also a leveraged play on the global commodities cycle, offering dual exposure to domestic growth and export-driven momentum.

Source : https://tradingeconomics.com/brazil/exports-by-category

II/ A Reliable Dividend Machine, Despite Some Irregularities

A/ Banco do Brasil’s Accounts Reflect a Bet on Brazil and commodities’ market

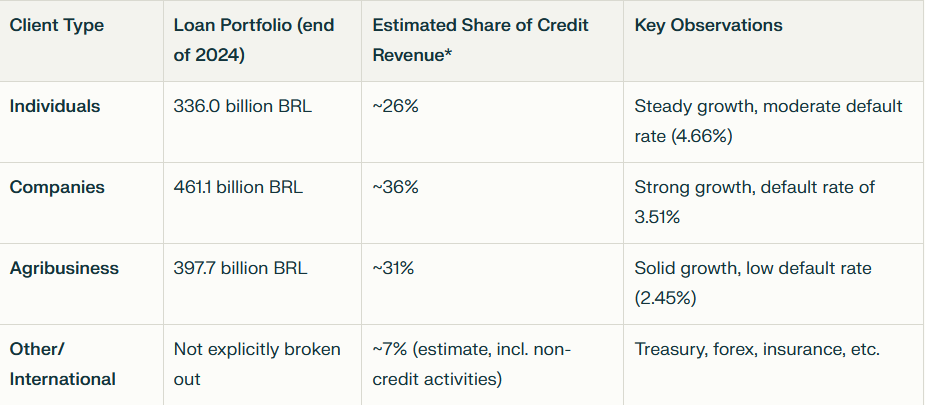

Banco do Brasil (BBAS3, BDORY) generates its revenue across a diverse set of sectors and client segments, reflecting its broad footprint in the Brazilian financial landscape. Banking remains by far the major activity.

In 2024, the bank reported total revenues of 102.27 billion BRL, with approximately 35% derived from retail banking, serving individual clients with loans, mortgages, and personal accounts. Corporate banking contributes around 30%, catering to medium and large enterprises, while agricultural financing—a cornerstone of its identity—accounts for 20%, driven by loans to farmers and agribusinesses tied to Brazil’s commodity exports. The remaining 15% stems from other activities, including insurance through BB Seguridade, investment banking, and digital services, highlighting the bank’s efforts to diversify beyond traditional lending.

This segmentation underscores Banco do Brasil’s reliance on both individual and institutional clients, with a notable emphasis on agriculture as a competitive advantage.

This revenue distribution offers insights into how Banco do Brasil’s activities align with, or diverge from, the broader Brazilian economy. Agriculture, representing 20% of the bank’s revenue, mirrors Brazil’s economic reliance on commodities, where the sector contributes about 21% to GDP according to recent IBGE data, suggesting a balanced representation. However, retail banking (35%) exceeds the economy’s consumer-driven activity (around 25% of GDP), indicating an overrepresentation as the bank taps into a growing middle class. Corporate banking (30%) aligns closely with the industrial and services sectors (approximately 30% of GDP), while the 15% from insurance and digital services slightly underrepresents the rising tech and financial services sector (around 20% of GDP). This suggests Banco do Brasil leans heavily on traditional strengths like agriculture and retail, potentially underinvesting in emerging digital opportunities compared to the economy’s evolving structure, a point worth monitoring for long-term growth.

B/ As an Investor, What Can I Observe?

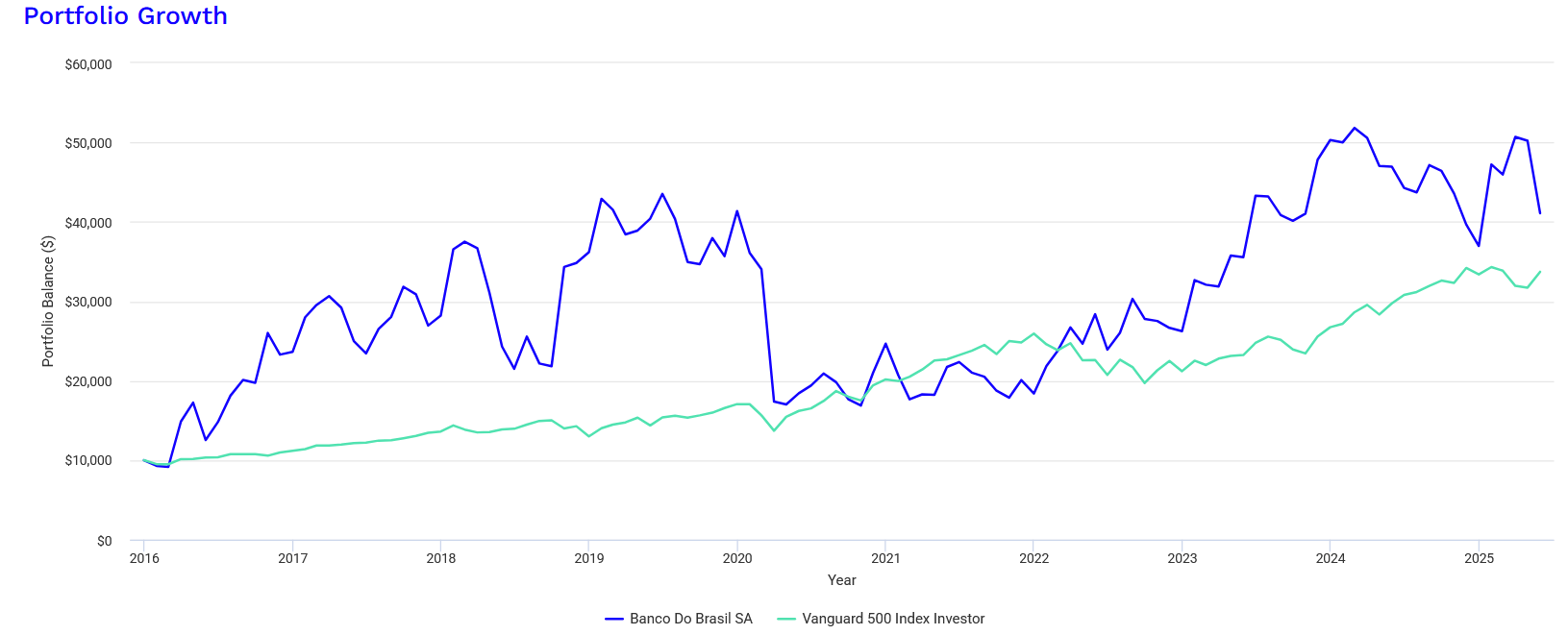

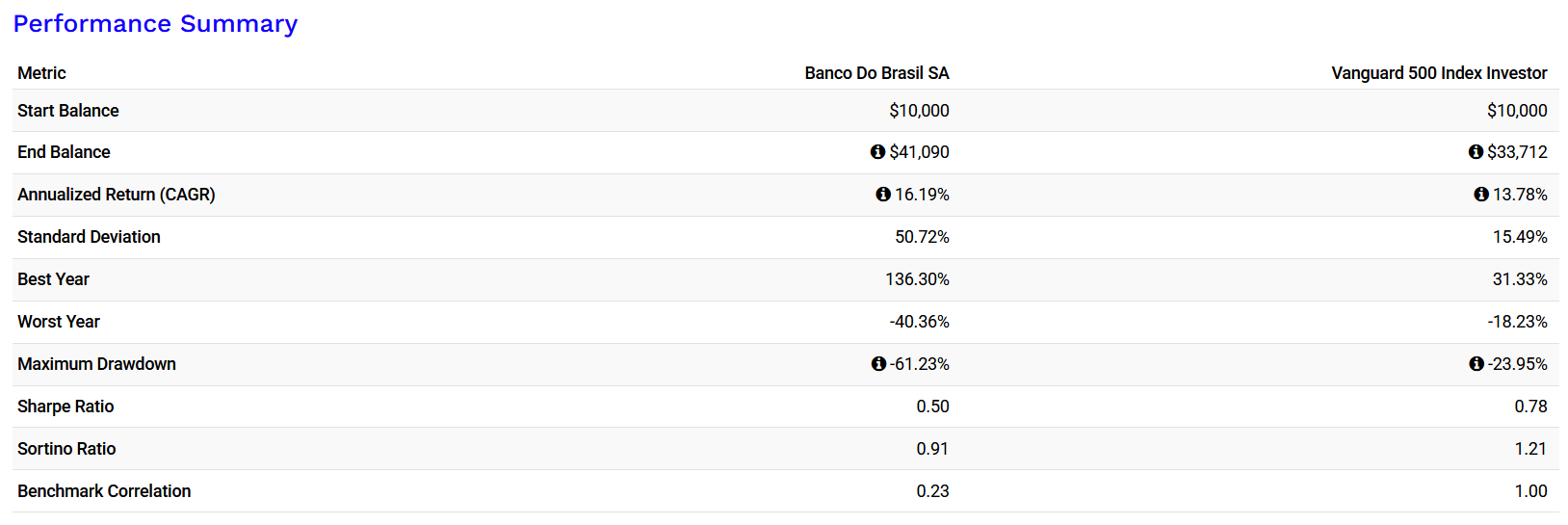

First, Banco do Brasil, since 2016, outperforms the S&P 500. I’m not sure it can outperform in the long term, but it’s already a solid starting point. There is a price to pay. See the chart below:

Source: Portfolio Visualizer

Thanks for reading! Subscribe for free to receive new posts and support my work.

As shown more clearly below, the main price to pay is the volatility of the stock price. The standard deviation from 2016 to 2025 is 50.72% for Banco do Brasil versus 15.49% for the S&P 500.

Source: Portfolio Visualizer

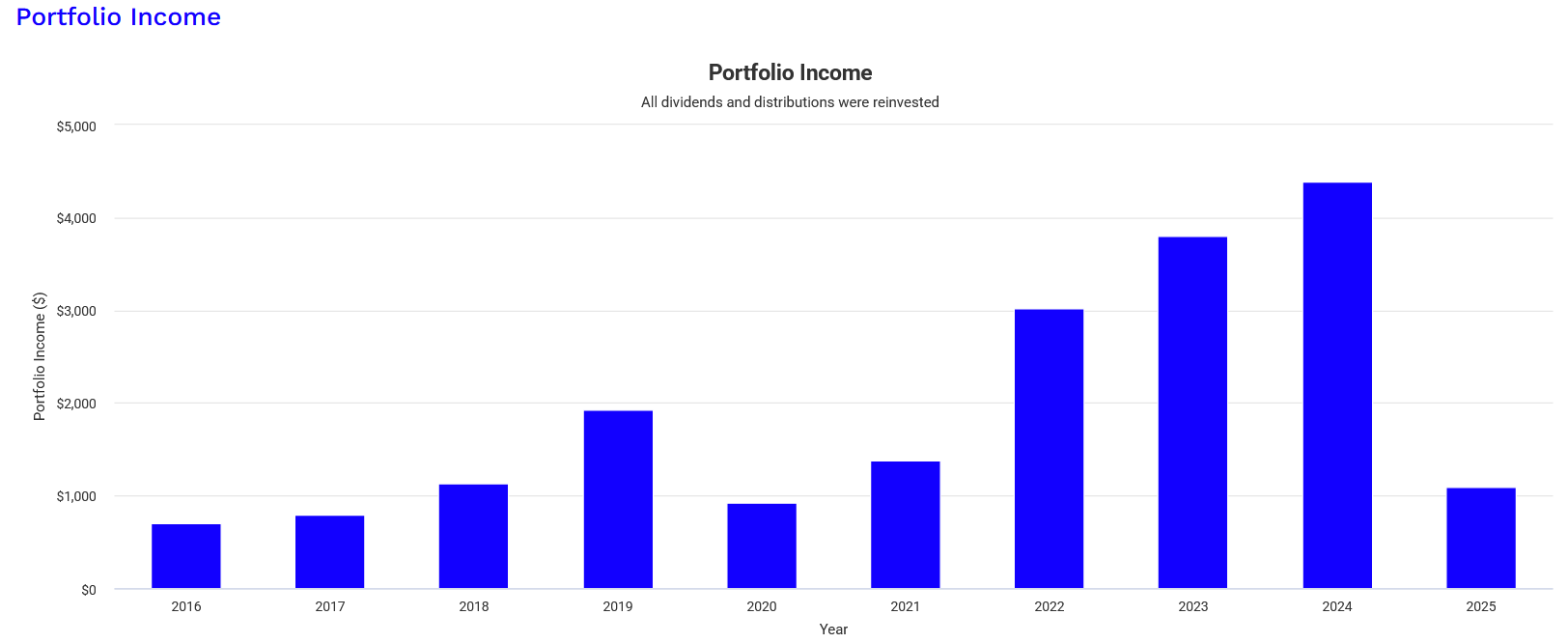

For an income investor, another aspect to keep in mind is that dividends are consistent but also cyclical, reflecting the structure of the Brazilian economy. This is the trade-off for strong performance and a high dividend yield. In the high yield world, there’s no free lunch.

Source: Portfolio Visualizer

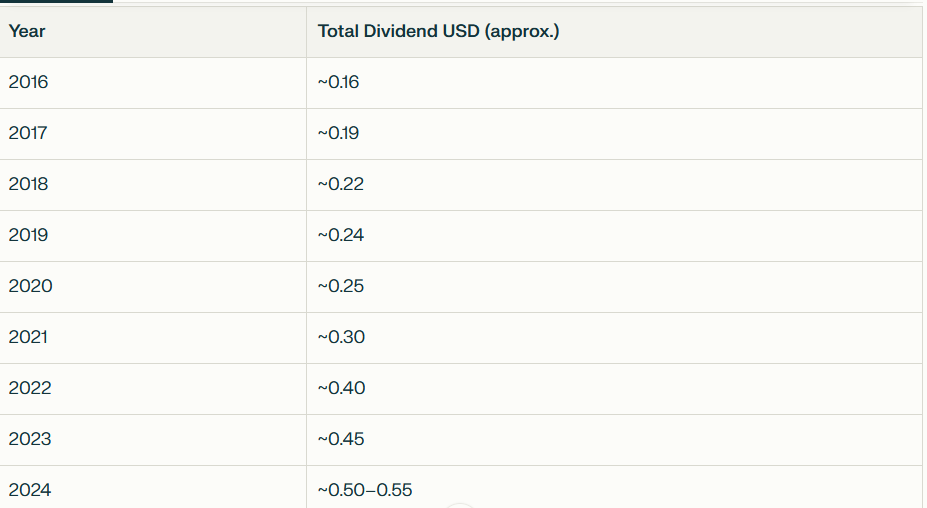

Banco do Brasil currently offers a dividend yield of around 10%, making it one of the most attractive income plays in emerging markets. It is quite hard to calculate because dividends are volatile. A dividend yield of over 10% might raise eyebrows in developed markets, but in Brazil, where real interest rates remain elevated and banks are used to navigating economic cycles, such yields—while not guaranteed—can be sustainable. Banco do Brasil’s payout reflects not distress, but a strong earnings base and conservative credit policies.

Conclusion – Investment Takeaways

In Part 1, we’ve focused solely on the macro aspects of Banco do Brasil. Next week, in Part 2, we’ll address the specific risks of this stock (state ownership, currency fluctuations, commodity price swings, agricultural credit).

From a long-term perspective—most critical for my global income portfolio—Banco do Brasil is a strong candidate for my portfolio. It’s a bet on:

- The Brazilian economy, which is fairly diversified and growing;

- The global commodities market (agricultural and mineral), strongly correlated with global growth;

- The rising influence of the BRICS.

In the short term, the stock price is low, and as of June 2025, it’s a good entry point. The advantage of the stock’s volatility is that attractive entry points can appear regularly.

As of today, I hold a small position of 56 shares ($BDORY), but I plan to buy an additional $1,700 worth of this stock in the coming days, using dividends from my global income portfolio.

In Part 2, I’ll cover the key risks: state control, credit quality, and what could kill the dividend. Make sure you’re subscribed if you don’t want to buy yield and get burned.

Liked this Deep-Dive? Buy Me a Coffee!

Your support keeps this newsletter independent and research-driven. If this analysis saved you time or gave you a new investment idea, consider making a one-time donation. Every contribution helps me maintain part of the research free and accessible to everyone.