Diversifying investments across countries is a well-known strategy, but many investors still don’t take full advantage of it. Even as global financial markets grow more connected, people around the world—whether in large economies like the U.S. or smaller, open ones like Canada—tend to favor local assets. This preference, called home bias, comes from a mix of comfort with the familiar and practical reasons. While there are valid explanations for focusing on domestic markets, the costs of missing out on global opportunities—lower risk and better returns—are often too high to ignore. Let’s explore why home bias persists and how spreading your investments worldwide can strengthen your portfolio.

Thanks for reading! Subscribe for free to receive new posts and support my work.

Home bias happens when investors put far more money into their own country’s assets than a balanced, global portfolio would suggest. Why does this happen? People naturally gravitate toward what feels familiar—local companies they read about or hear discussed in the news. Investing abroad can also seem daunting due to currency fluctuations, higher fees, or tax rules, like those affecting foreign dividends or benefits for staying local. Plus, regulations and limited information about overseas markets can make international investing feel out of reach.

B. Professional Investors Are Looking Beyond Borders

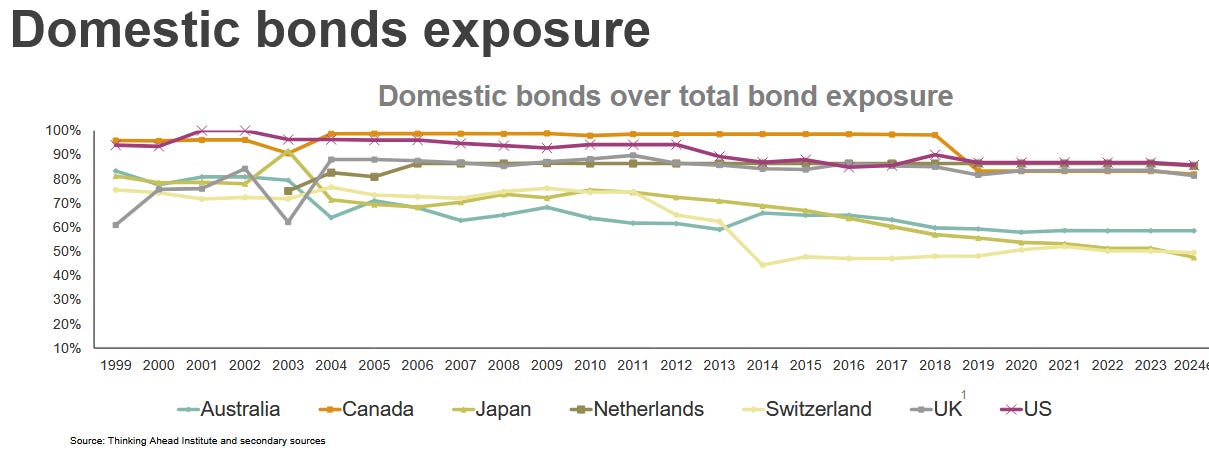

Over the past 20 to 30 years, large investors like pension funds and sovereign wealth funds have shifted their approach. They’ve reduced their focus on domestic stocks, with the average share of local equities in their portfolios dropping from 57.1% in 2004 to 34.1% in 2024. This shows a clear move toward global markets. Bonds, however, remain more tied to home markets, influenced by regulations and long-standing preferences.

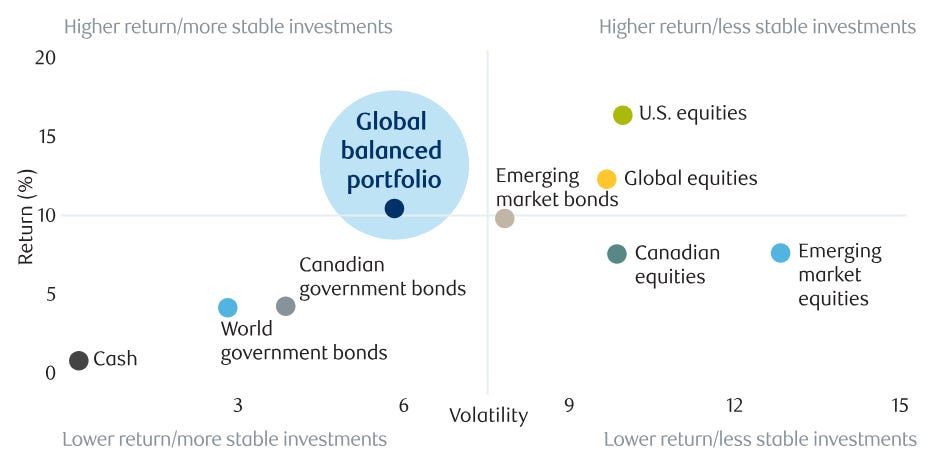

Investing in markets beyond your home country helps protect your portfolio by reducing reliance on a single economy’s performance. It also opens opportunities to capture stronger returns from growing markets worldwide. According to a 2014 study published in ScienceDirect titled “The Benefits of International Diversification for US Investors,” U.S. investors who combined S&P 500 stocks with international equities reduced portfolio volatility by 15-20%. This diversification also improved the Sharpe ratio, a measure of how much return you earn for the risk you take—a higher ratio means a more efficient portfolio (ScienceDirect, 2014).

A 2024 study, “International Portfolio Diversification Benefits,” published in Sciendo, analyzed 28 European markets from 2014 to 2019 and found that diversification cut portfolio volatility by 47.2%. This reduction came from exposure to high-growth sectors, such as U.S. technology or emerging markets. For Canadian investors, global diversification offers a way to stabilize income by balancing out fluctuations in domestic markets, as highlighted in RBC Global Asset Management’s “Global Investment Outlook” (RBC Global Asset Management, 2024).

So, how can you put these insights to work? Let’s dive into the details.

II. Why You Can’t Rely on Just One Country or Currency

A. The Case for Going Global

Focusing investments on a single country or currency increases exposure to local economic volatility, limiting potential returns. Global diversification reduces risk and unlocks opportunities in dynamic markets worldwide. Below, we explore how investors in three regions—North America, Europe, and Asia—can benefit from international strategies, separating macroeconomic risks from actionable investment opportunities, with evidence and examples.

Currency volatility can also work in favor of U.S. investors (USD)

Macroeconomic Context: The U.S. dollar’s dominance, representing 60% of global foreign exchange reserves (International Monetary Fund, 2024), can create a false sense of security. In 2022, a 10% dollar appreciation reduced the competitiveness of U.S. exports and pressured corporate earnings, impacting domestic market performance (International Monetary Fund, 2024).

Investment Opportunities: Diversifying into international markets mitigates these risks and enhances returns. A 2014 study, “The Benefits of International Diversification for US Investors,” found that adding European or Japanese assets to a U.S. portfolio reduced volatility by 15-20% over the long term (ScienceDirect, 2014). For example, in July 2022, when the euro was at a low of 0.95 USD, investing in the MSCI Europe ETF (iShares, ticker: IEUR) captured a 12% European market rebound in 2023, outperforming a U.S.-only portfolio over two years. The following provides an overview of the current currency landscape.

European investors (EUR) can turn the euro’s structural weaknesses into an opportunity

Macroeconomic Context: Eurozone investors face risks from regional economic disparities, such as Germany’s strength versus Greece’s economic challenges. The 2011 eurozone debt crisis caused a 15% depreciation in the euro’s value within months, adversely affecting local portfolios (European Central Bank, 2024).

Investment Opportunities: Global diversification helps shield against such volatility. A 2024 study, “International Portfolio Diversification Benefits,” showed that incorporating U.S. assets into European portfolios reduced volatility by 47.2% from 2014 to 2019 (Sciendo, 2024). For instance, in August 2011, when 1 EUR equaled 1.40 USD, an investment in the S&P 500 ETF (iShares, ticker: IVV) delivered an 80% return over the decade from 2011 to 2021, significantly outpacing European markets.

Macroeconomic Context: Investors in Japan and China contend with currency volatility and structural constraints. In 2022, the Japanese yen weakened by 20% against the USD, while China’s tightly controlled yuan restricted flexibility, particularly in Japan’s low-growth economy (International Monetary Fund, 2024).

Investment Opportunities: Diversifying into U.S. or European markets reduces these risks. The 2014 ScienceDirect study indicated that adding U.S. or European assets to Asian portfolios lowered volatility by 15-20% (ScienceDirect, 2014). For example, in October 2022, when 150 JPY equaled 1 USD, an investment in the Euro Stoxx 50 ETF (iShares, ticker: EUE) gained 10% in 2023, while Japan’s Nikkei 225 index fell by 5%.

These cases demonstrate how global diversification protects against regional economic risks while improving portfolio performance.

B. The Strategic Imperative of Global Diversification

A domestic-only investment approach exposes portfolios to unique risks and missed opportunities that can undermine long-term performance. Global diversification not only mitigates these challenges but also positions investors to benefit from international markets’ resilience and growth. Below, we explore three critical reasons to diversify internationally: protection against country-specific market crashes, capturing high-growth opportunities in other regions, and addressing structural currency risks.

Tail Risk: Protection from Country-Specific Crashes Investing heavily in one country leaves portfolios vulnerable to localized crises, such as economic collapses or political turmoil. In 2015, Greece’s debt crisis triggered a 50% plunge in the Athens Stock Exchange General Index, devastating local investors. Meanwhile, globally diversified portfolios, including developped and emerging market assets, were less affected due to uncorrelated market movements. For example, an investor holding the iShares MSCI World ETF, which tracks global markets, saw losses limited to under 10% during the 2015 Greek crisis, compared to Greece’s 50% drop for a euro investor. Diversification acts as a buffer against such tail risks, as seen during the 2020 pandemic when global markets recovered at varying rates.

Opportunity Cost: Capturing High-Growth Markets Limiting investments to your home market can mean missing out on sustained growth in dynamic economies. From 2010 to 2020, India’s equity market, tracked by the MSCI India Index, delivered an annualized return of 8.2%, outpacing many developed markets like Japan (4.1% annualized, Nikkei 225) and Europe (5.6% annualized, MSCI Europe). Investors who overlooked India missed significant gains, particularly in technology and consumer sectors. For instance, the iShares MSCI India ETF, launched in 2012, gained approximately 60% from 2012 to 2020, compared to Japan’s Nikkei 225 at 40%. Allocating to high-growth markets like India over the long term enhances portfolio performance.

Source : investing.com

Structural Risks: Anticipating Currency Challenges Over-reliance on a single currency exposes investors to long-term structural risks, such as shifts in global currency dominance or weaknesses in smaller currencies. The U.S. dollar, while currently holding 60% of global foreign exchange reserves (International Monetary Fund, 2024), faces potential challenges from rising alternatives like the euro or yuan, as global trade patterns evolve. Similarly, smaller currencies, like the Swedish krona or South African rand, are prone to volatility due to limited economic scale. For example, the rand depreciated by 12% against the USD in 2023, eroding returns for South African investors focused domestically. Diversifying into a basket of currencies through international assets protects investors from these countries.

In theory, everyone agrees on diversification. In practice, most portfolios stay stuck in the past—domestic-heavy, currency-concentrated, and overly dependent on a single economy. Now we need practical tools (read part 2 next week).

A world map to track underpriced regions

A currency tracker to monitor trends

A clear set of benchmarks for global and sector diversification

Whether you’re building wealth or seeking a steady stream of income, breaking out of the home bias trap isn’t just smart—it’s essential.

🌐 In a world where shocks are global, your portfolio better be too. And you need tools like this one:

Liked this Deep-Dive? Buy Me a Coffee!

Your support keeps this newsletter independent and research-driven. If this analysis saved you time or gave you a new investment idea, consider making a one-time donation. Every contribution helps me maintain part of the research free and accessible to everyone.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or legal advice. The views expressed are personal opinions and should not be taken as specific recommendations. Investing involves risks, including the potential loss of capital. Always conduct your own research and consult a qualified financial advisor before making any investment decisions. The author is not responsible for any financial losses or decisions based on the content of this article.